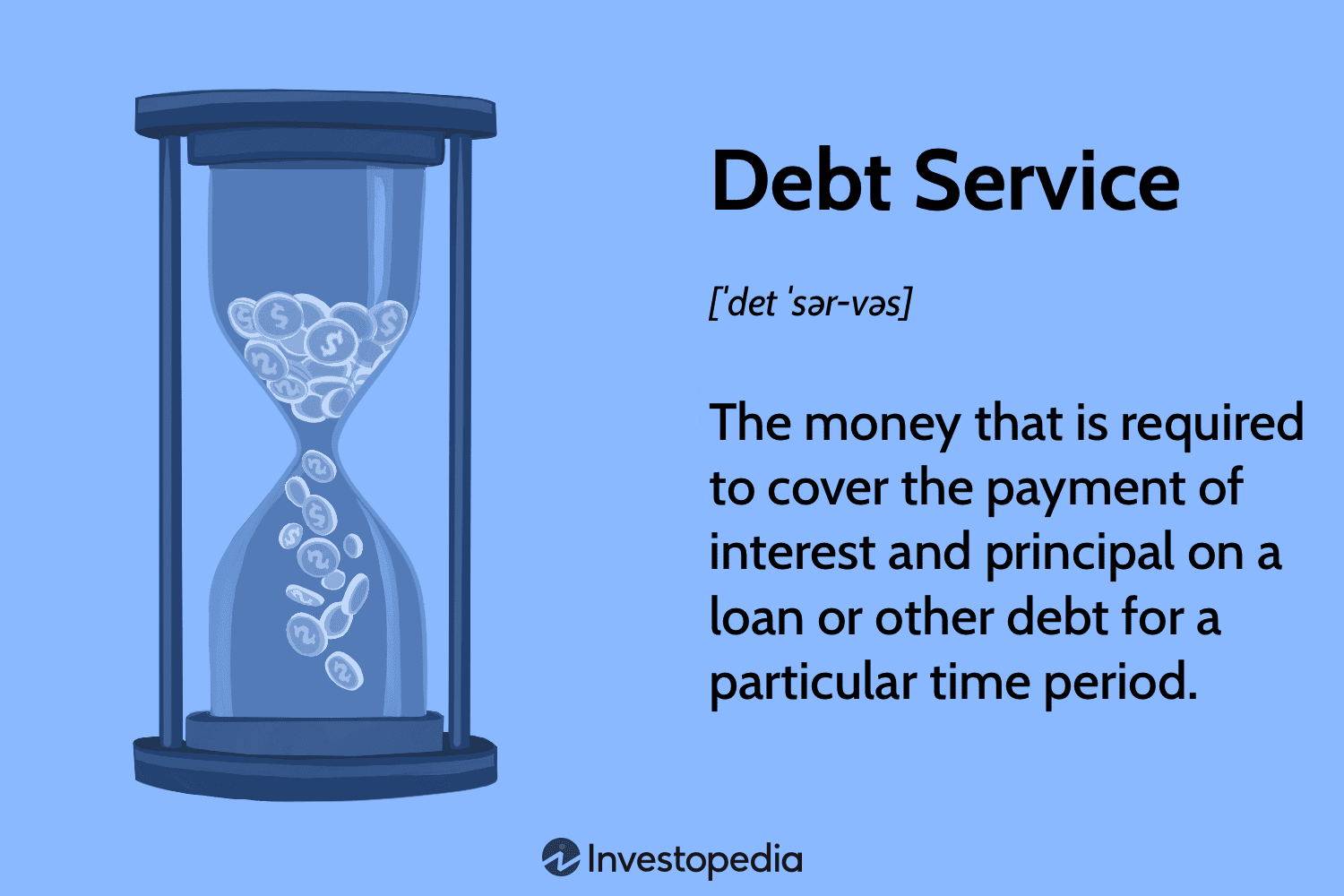

Individual and business finance frequently view debt as a necessary evil. Effectively handling financial debt – be it it is a home loan, business loan or credit card debt – is crucial to economic stability and development. One key element of debt management is understanding different debt service types and selecting the one which best fits your circumstances and needs. We will examine various debt service options in this particular blog post and decide which one is most suitable for you.

Individual and business finance frequently view debt as a necessary evil. Effectively handling financial debt – be it it is a home loan, business loan or credit card debt – is crucial to economic stability and development. One key element of debt management is understanding different debt service types and selecting the one which best fits your circumstances and needs. We will examine various debt service options in this particular blog post and decide which one is most suitable for you.

Debt Service at a fixed rate:

Fixed-rate debt service entails paying a constant amount of interest and principal throughout the lifetime of the loan. This particular kind of debt service offers predictability and stability since your monthly payments remain the same regardless of fluctuations in interest rates. It’s particularly suitable for individuals as well as companies who prioritize budgeting and wish to stay away from surprises in their cash flow.

Variable-rate Debt Service:

Unlike fixed rate debt, variable rate debt service entails interest rates which can fluctuate over time, generally consistent with market interest rates. Although initial payments might be lower as compared to fixed rate loans, there’s a threat of payments increasing if interest rates rise. Variable-rate debt service may be useful when interest rates are very low but could pose a challenge when rates increase considerably.

Debt Service with Interest Only:

Interest-only debt service entails borrowers paying just a set amount of interest for a predetermined time frame, typically in the start of the loan period. This particular kind of debt service could provide greater flexibility, lower first payments and might be appropriate for borrowers anticipating potential cash flow. It is important to remember that after the interest free period concludes, payments will rise, possibly increasing overall costs.

Balloon Payment Debt Service:

The debt service model referred to as balloon payment consists of making reduced monthly payments over the loan period, with a substantial last payment (the “balloon payment”) due at the conclusion of the loan term. This particular kind of debt service may be appealing for borrowers that plan to have substantial money available in case the balloon payment is due, such as through the sale of an asset or an anticipated increase in earnings. Nevertheless, not planning for the balloon payment can result in financial strain or the need to refinance.

Amortizing Debt Service:

Amortizing debt service entails repaying both interest and principal during the loan term through identical regular payments. Home mortgages and installment loans usually use this form of debt service. With every payment, a portion goes towards decreasing the principal balance, leading to gradual debt reduction. The procedure of amortizing debt service offers clarity and guarantees repayment of the loan in full at the conclusion of the term.

What debt service type is most suitable for you? The answer will differ according to your financial objectives, risk appetite, cash flow projections and market conditions. It’s crucial to thoroughly assess your options and talk with financial advisors if needed to make an educated decision.

Fixed-rate debt service may be a good option in case you value stability and predictability. Variable-rate or interest-only debt service might be a great choice in case you are prepared to accept a little uncertainty and take advantage of potential rate variations.

Ultimately, the answer is to pick a debt service type which fits with your financial situation as well as long-term objectives while simultaneously weighing possible risks and contingencies. It is possible to make confident financial choices by knowing the advantages and drawbacks of each choice as well as doing comprehensive research to guarantee its viability.